As the name suggests, it’s a phenomenon that impacts homeowners who purchased a property and then fixed the rate on their mortgage – and according to the RBA, it’s going to come into play for hundreds of thousands of Australians in 2023.

So what actually is the fixed rate mortgage cliff, and how is it going to affect the economy this year?

What is the fixed rate mortgage cliff?

The fixed rate mortgage cliff describes when people on fixed interest rate home loans come to the end of the period when their rate is locked in, and therefore get hit by an unusually high jump in repayments.

This is exactly what is about to happen to hundreds of thousands of Australians with home loans.

Around the time the cash rate dropped to its historic low of 0.10 per cent in November 2020, many Aussies took advantage by securing a fixed-rate loan to buy property.

However, because the rate is not fixed for the entirety of the loan and instead only a short period – generally in Australia it’s five or fewer years – many are now about to be hit by all of the recent interest rate hikes in one go.

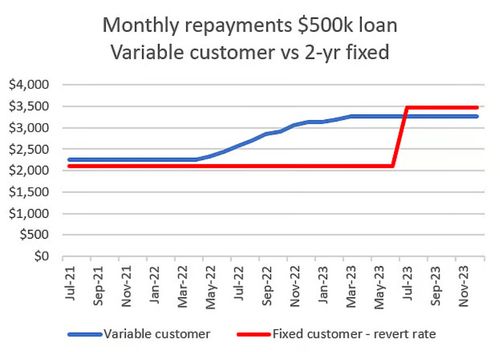

Contrast that to variable rate customers, and you can see why the phenomenon is described as a cliff:

How many borrowers in Australia will be impacted this year?

We don’t know precisely how many Australians are heading towards the cliff this year, but the RBA estimates the number isn’t far off a million.

“The number which you would be looking at is somewhere in the high 800,000s,” Marion Kohler, the head of the RBA’s economic analysis department, said when asked about the number of fixed rate loans “rolling off” in 2023 by the Senate Select Committee on the Cost of Living on February 1.

“But that is not necessarily 800,000 households; there are people who have more than one loan facility… so it’s likely to be a little less, but that’s a really rough, ‘back of the envelope’ calculation as I understand it from the team.”

Kohler said that equates to about $350 billion in credit rolling off from fixed to variable interest rates in 2023.

Will people default on their loans?

With fixed-rate borrowers set to be hit by monthly repayment increases of $1000 and more, there is concern that some people may not be able to afford their mortgages anymore.

While some borrowers may end up defaulting on their home loans, it is likely that the majority will tighten their belts, cutting back on other spending so they can afford their repayments.

Read Related Also: Khloe Kardashian Sued By Former Assistant Over Unpaid Wages

That will have a flow-on effect on the wider economy – one that is already evident in current forecasts. In the RBA’s February 2023 statement on monetary policy, its predicted economic growth will go from 2.75 per cent in 2022 to 1.5 per cent for both 2023 and 2024.

Sign up here to receive our daily newsletters and breaking news alerts, sent straight to your inbox.

What can people do to prepare for a fixed rate increase?

If you’re on a fixed rate loan and are approaching rolling off to variable rates, RateCity CEO Paul Marshall says it’s critical to act.

“The worst thing you can do is nothing,” he said.

“When your fixed term home loan is coming to end, make sure to seriously consider your options.”

Taking out a new fixed term loan is an option – although Marshall notes there are drawbacks.

“Not every lender will allow you to re-fix your loan, or allow you to do so multiple times, so you may need to switch lenders to stay on a fixed rate,” he said.

“And since the cash rate has changed significantly since you last fixed your loan, you should be prepared for higher fixed rate options this time around.”

You could also look at splitting your mortgage between fixed and variable rates, or shop around for a cheaper variable rate than the one your existing lender will offer.

”You could consider contacting your bank and ask them to switch you to a lower rate,” he said.

“The bank may be willing to make concessions in order to keep you as a customer. Staying with the same lender could save you the hassle of moving your mortgage elsewhere.

“If your lender can’t or won’t make you a deal, you could consider taking your ball and going home and switching to a different lender. Some mortgage lenders are eager to secure the business of refinancers, and are willing to not only offer discounted interest rates, but other features and benefits such as cashback deals.”

The top 10 highest paying jobs in Australia where you don’t need a degree

The information provided on this website is general in nature only and does not constitute personal financial advice. The information has been prepared without taking into account your personal objectives, financial situation or needs. Before acting on any information on this website you should consider the appropriateness of the information having regard to your objectives, financial situation and needs.